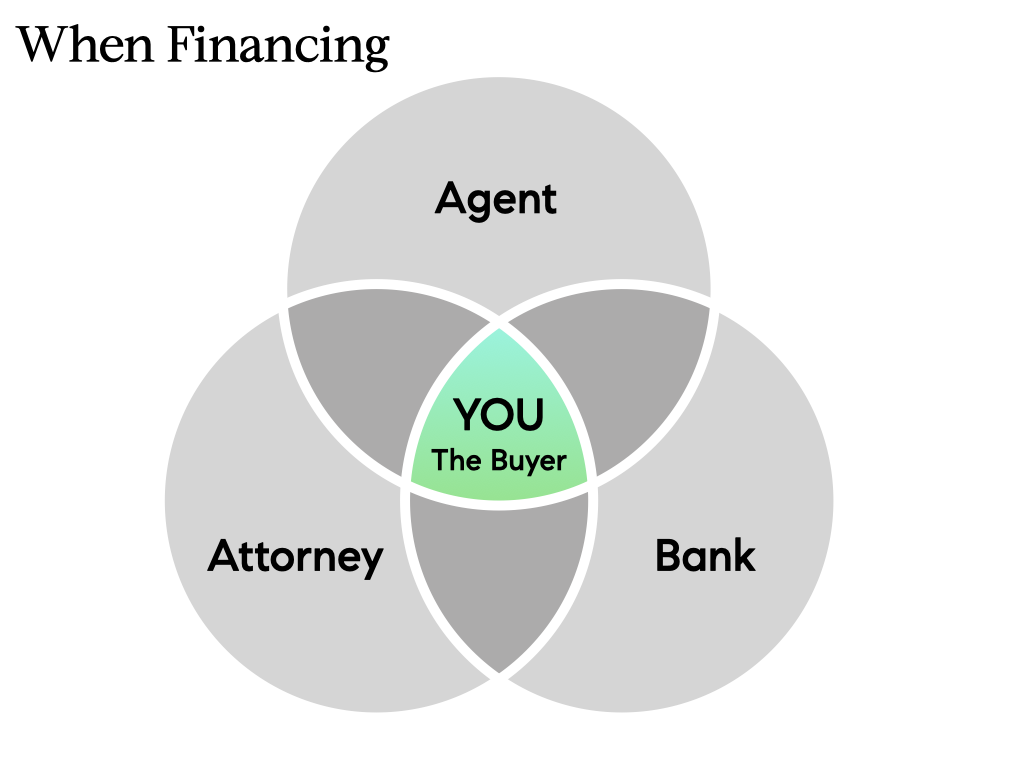

If you are financing, now is the time to shop Lenders. You are officially In Contract, which means banks take you seriously. Lenders will compete for your business. See what they can offer.

If you shop your contract, get competing quotes within 10 calendar days — to be extra safe.

PRO TIP: You have a 14-Day Window to Run Credit Safely.

Optimal shopping period time frames are built around FICO scoring models so get all of your Pre-Approvals done in 2 weeks. FICO should give you a 14-day grace period for mortgages. In other words, FICO treats similar loan-related inquiries within 14 days of each other as a single inquiry.

The Purchase App

If you’re buying in a Condominium or Cooperative, you’re going to need to submit a Purchase Application (Also called a “Board Application”). We pride ourselves on our expertise with Purchase Applications, so we’ve got you covered.